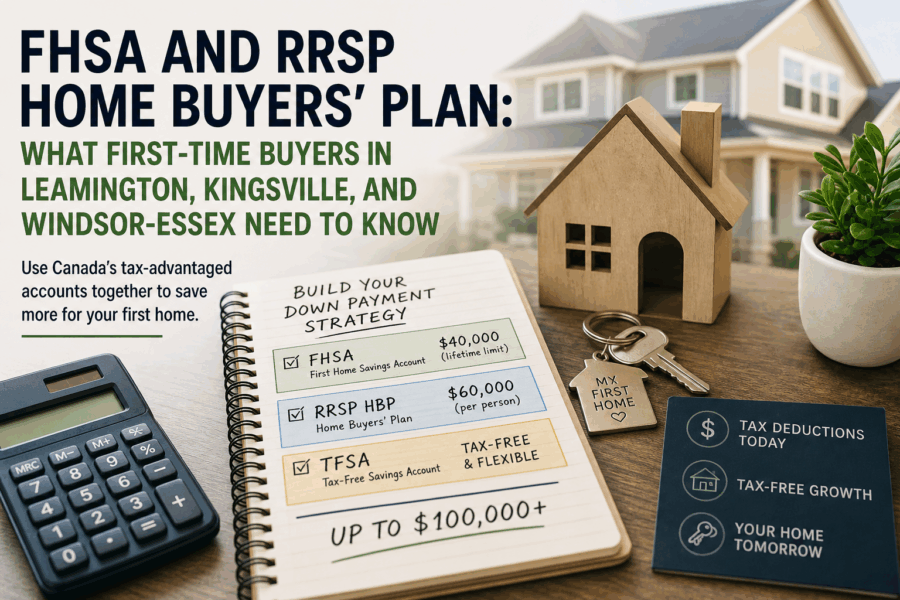

What is the best way for first-time buyers in Windsor-Essex to save for a home? Two federal programs — the First Home Savings Account (FHSA) and the RRSP Home Buyers’ Plan — can be used together to give first-time buyers in Leamington, Kingsville, Wheatley, and across Windsor-Essex up to $100,000 in tax-advantaged savings toward a down payment. Many buyers also bring TFSA savings to the table on top of that.

If you’re thinking about buying your first home in southwestern Ontario, you’ve probably heard all three of these names. Maybe you’ve looked them up. But there’s a difference between knowing the programs exist and actually understanding how they work well enough to use them strategically. That’s what this post is for.

Here’s a plain-language breakdown of all three, how they differ, and how first-time buyers in our region can put them together.

The First Home Savings Account (FHSA): The Newer, More Flexible Option

The FHSA was introduced by the federal government in 2023, and it’s still one of the least-used tools available to first-time buyers — mostly because a lot of people simply don’t know enough about it yet.

Here’s the short version: you contribute money to your FHSA, get a tax deduction for that contribution (like an RRSP), and when you eventually withdraw the funds to buy a qualifying home, the withdrawal is completely tax-free — no repayment required (like a TFSA). No other registered account in Canada offers both of those benefits at the same time.

The contribution limits are $8,000 per year and $40,000 over your lifetime. Unused room carries forward — up to $8,000 per year — so if you can only contribute $5,000 this year, you’ll have up to $11,000 of room available next year. That carry-forward room starts accumulating from the date you open the account, not from your first deposit.

That last point matters. If you’re even thinking about buying a home in the next few years, open your FHSA now. Even if you can’t put money in immediately, the clock on your carry-forward room is already ticking from opening day.

If you open an FHSA and ultimately never buy a home, the balance can be transferred to your RRSP or RRIF on a tax-deferred basis within 15 years. You won’t lose the savings.

Government resource: First Home Savings Account (FHSA) — Canada Revenue Agency

The RRSP Home Buyers’ Plan (HBP): The Established Option With One Key Condition

The RRSP Home Buyers’ Plan has been around since 1992, which is why most people have at least heard of it. But the rules have changed more recently than many buyers realize.

As of April 2024, the HBP withdrawal limit was raised to $60,000 per person, up from $35,000. For a couple buying together where both qualify, that’s up to $120,000 from RRSPs alone.

The mechanics are different from the FHSA. You withdraw from your RRSP tax-free at the time of purchase — but you’re essentially borrowing from your own retirement savings, and the amount has to be repaid to your RRSP over 15 years, starting two years after the year you withdrew. Miss a scheduled repayment in any given year and that missed amount gets added to your taxable income.

There’s also a timing rule that catches a lot of buyers off guard: the funds you plan to withdraw must have been sitting in your RRSP for at least 90 days before you can use them under the HBP. If you move money in and try to use it right away, you won’t qualify. Build that 90-day window into your timeline.

What About a TFSA? It Can Help Too

The Tax-Free Savings Account isn’t a dedicated home-buying program — it has no special first-time buyer rules, no annual contribution limit tied to home purchase, and no repayment schedule. But that doesn’t mean it’s irrelevant. Many first-time buyers arrive at the closing table with a meaningful portion of their down payment sitting in a TFSA, and there’s a very good reason for that.

Any money you withdraw from a TFSA is completely tax-free, at any time, for any purpose. There are no forms to fill out, no qualifications to meet, and no conditions on how the funds are used. If you’ve been saving in a TFSA for a few years and have $20,000 or $30,000 built up, you can put that straight toward your purchase without a second thought.

The TFSA contribution limit has grown every year since the account launched in 2009. As of 2025, the cumulative lifetime contribution room for someone who has been eligible since the program started is $95,000. If you haven’t maximized your TFSA yet, it’s worth knowing how much room you have — the CRA My Account portal will show you your available room.

The practical takeaway: think of the TFSA as a flexible complement to your FHSA and HBP strategy, not a replacement. If you have TFSA savings already built up, they can supplement the funds you draw from your other accounts. If you’re still building your savings and need to prioritize, the FHSA is generally the stronger dedicated home-buying vehicle because of the combined tax deduction and tax-free withdrawal.

FHSA vs. RRSP Home Buyers’ Plan vs. TFSA: The Key Differences

| FHSA | RRSP Home Buyers’ Plan | TFSA | |

|---|---|---|---|

| Maximum amount | $40,000 lifetime | $60,000 | No cap on withdrawal |

| Tax deduction on contributions | Yes | Yes (RRSP contributions) | No |

| Withdrawal is tax-free | Yes | Yes | Yes |

| Repayment required | No | Yes, over 15 years | No |

| 90-day holding rule | No | Yes | No |

| Purpose restriction | Home purchase only | Home purchase only | Any purpose |

| Unused room carries forward | Yes (up to $8,000/yr) | N/A | Yes (accumulates from 2009) |

Can You Use All Three for the Same Purchase?

Yes — and this is where things get interesting for buyers in Windsor-Essex and Chatham-Kent.

The Canada Revenue Agency confirms you can make a qualifying FHSA withdrawal and an RRSP HBP withdrawal for the same home purchase, as long as you meet the conditions for each account at the time of withdrawal. Add in whatever TFSA savings you’ve accumulated, and a well-prepared buyer can combine all three sources toward a single down payment.

The order most financial advisors suggest: FHSA first (no repayment obligation), then HBP for any remaining amount needed, with TFSA funds filling any remaining gap. This keeps your future repayment obligations as small as possible and your retirement savings as intact as possible.

What Does This Mean for Buyers in Windsor-Essex and Chatham-Kent?

Here’s where it gets practical for our market. Windsor-Essex and Chatham-Kent remain among the most accessible entry points for first-time buyers in Ontario. Median home prices in communities like Leamington, Kingsville, and Wheatley are a fraction of what buyers face in the GTA — which means $40,000 to $100,000+ in down payment savings through these programs goes a long way here.

If you’re a first-time buyer relocating from a higher-cost market, or a younger buyer who grew up in the region and wants to stay close to home, the combination of these programs and our local price points can make ownership very achievable. A fully funded FHSA, a solid HBP withdrawal, and a few years of TFSA savings can realistically cover a meaningful down payment on a home in Leamington or Kingsville without forcing you to over-extend.

One more thing worth knowing right now: if you’re considering a newly built home, Ontario and the federal government introduced a temporary HST rebate on new homes priced under $1 million, effective April 1, 2026 through March 31, 2027. That’s potential savings of up to $130,000 on top of your down payment programs. If new construction is on your radar, it’s worth factoring in.

And if you haven’t sorted out your mortgage pre-approval yet, that’s the natural next step once your savings strategy is in place. Here’s more on arranging financing and what lenders look for.

A Simple Action Plan

- Open your FHSA today — even before you can contribute. Carry-forward room starts from your opening date.

- Contribute up to $8,000 per year and claim the deduction each tax year. Monthly contributions around $667 keep you on pace.

- Build your RRSP separately and make sure the funds you plan to use under the HBP have been in the account for at least 90 days before you need them.

- Check your TFSA contribution room via CRA My Account and consider directing additional savings there — it gives you tax-free flexibility on whatever you don’t end up pulling from your FHSA or RRSP.

- When you’re ready to buy, withdraw from your FHSA first (Form RC459), then from your RRSP if needed (Form T1036). Your mortgage professional or real estate lawyer can help coordinate the timing.

- Plan your HBP repayments in advance. Know when the repayment window opens and set up an automatic RRSP contribution so you’re never caught with an unpaid amount added to your income.

Frequently Asked Questions

Can I use both the FHSA and the RRSP Home Buyers’ Plan to buy a home in Windsor-Essex? Yes. The CRA permits qualifying withdrawals from both accounts for the same home purchase, as long as you meet the conditions for each at the time of withdrawal. Most buyers are advised to use FHSA funds first since there’s no repayment obligation, then supplement with the HBP for any remaining amount needed.

How much can I withdraw tax-free using these programs as a first-time buyer in Ontario? Up to $40,000 from your FHSA (lifetime limit) and up to $60,000 from your RRSP under the Home Buyers’ Plan — for a combined maximum of $100,000 per person. For couples where both qualify, that’s up to $200,000 combined. TFSA savings can supplement this further with no cap on the withdrawal amount.

Can I use my TFSA for a down payment on a home in Leamington or Kingsville? Yes. TFSA withdrawals are completely tax-free, with no conditions on how the funds are used and no repayment requirement. There’s no dedicated TFSA home-buying program, but many buyers use accumulated TFSA savings to supplement their FHSA and HBP funds for the same purchase.

What if I open an FHSA but end up not buying a home? If you don’t use the funds for a qualifying home purchase within 15 years of opening the account, the full balance can be transferred to your RRSP or RRIF on a tax-deferred basis. You won’t lose your savings — they simply shift to your retirement account.

Questions? Happy to Walk You Through It

Sorting out your financing strategy is one of the most important steps before buying your first home in Windsor-Essex or Chatham-Kent. I’m not a financial advisor, but I work with first-time buyers in Leamington, Kingsville, Wheatley, and across the region every day, and I can point you toward the right questions to ask and connect you with the right people.

Questions? I’m always happy to chat — no pressure, no obligation. Reach out at lindahakrrealtor.ca or give me a call.

About Linda Hakr, REALTOR® | Top 5% at Jump Realty | Wheatley & Windsor-Essex Real Estate Specialist. Linda Hakr is a Top Producer with JUMP Realty — Wheatley, Leamington, Kingsville, Windsor-Essex, Chatham-Kent. #1 Wheatley, #1 Leamington on RateMyAgent, 5 cities & 7 neighbourhoods. 39 five-star Google reviews, 100% response rate. 📞 519-654-6695 🌐 lindahakrrealtor.ca